The Quant's Toolkit

World class data and back-testing capabilities are now at the retail trader's fingertips. These tools are essential. Then, as traders become more sophisticated, they often overlook the importance of software for execution & portfolio management.

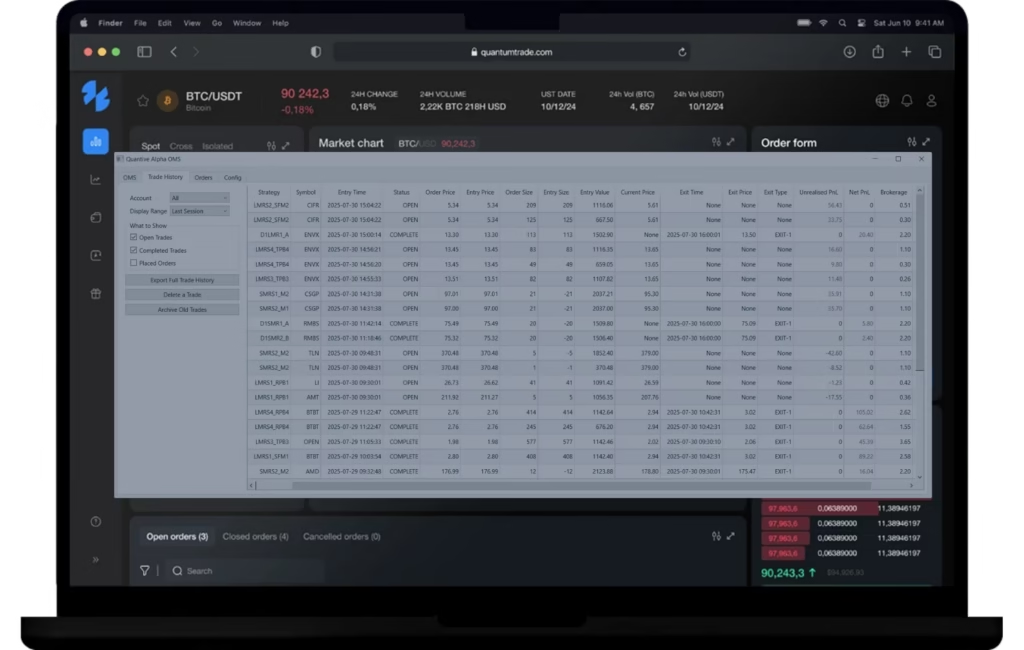

Yes, open source access to an extensive OMS with a truckload of features.

Algo Terminal

True Multi-Strat

Position Sizing

Track Every Trade

Advanced Features

Reporting & Alerts

For RT, Amibroker, Python

Harvest extra alpha

Expert execution

- International stocks & ETFs, including CFDs

- Futures

- Trade dozens of strategies, send hundreds of orders

Feature rich

- Record all trades, easily compare live to back-test

- Daily reporting, error reporting, performance reporting

- Reconciliation of strategies

Bonus: Telegram Bot

- Monitor live performance of your IB account from Telegram

- Daily, Month to Date & Year to Date returns, net of all deposits & withdrawals at your fingertips.

- Particularly useful for those who hedge their portfolio with futures, which makes the IB returns incorrect.

The Tools We Use

Opt My Strategy

From Trade Like a Machine

- For algo traders tired of “great” backtests that fail in live trading

- Built to expose overfitting — not reward it

- Engineered to avoid the subtle traps common in traditional optimization tools

- MetaTrader produces the raw optimization data - OMS identifies the true edge of your strategy

- Research Dashboards, Intelligent Strategy Edge Identification, Quant-Grade Strategy Analysis, Works with the MT4 and MT5 Strategy Testers

This tool created by Martyn Tinsley is essential for MT4/5 users, but every serious quant trader should read Martyn’s paper on Walk Forward Correlation Analysis, which can be found on his site here!

To learn more about Martyn’s process for creating robust strategies by design, I thoroughly recommend podcast episodes 52 & 53.

Generate random market data

- Generate random data for one or many contracts.

- Add 'trend', constrain range to immitate real contracts, etc.

- Test your strategy robustness. See podcast Ep 011 for a walk through!

- FREE for Algo Collective members

RealTest - backtesting & analysis

Simple yet powerful

Developed by Marsten Parker, the only systematic trader to appear in Jack Schwager’s Market Wizards books, we believe this product represents the single best value back-testing engine on the market.

Using an intuitive script syntax that is easy to learn, you’ll get moving quickly, particularly with the many sample scripts provided. Despite this simplicity, there is enormous power and functionality under the hood. Perhaps the fastest back-testing engine on the market, it is able to handle stocks, currencies and futures with ease. There’s also a vibrant and helpful community on the RealTest forum.

Key Features

- Multi-Strategy Modeling: combine multiple strategies across long/short, strategy type, market, bar size and view true portfolio based results and correlations easily.

- Actual Trade Testing: users can import actual trades and compare them against backtest results.

- Powerful Optimisation & Analysis Tools: including interval tests, walk-forward, monte-carlo, genetic optimisation and so on. There are powerful analysis tools that allow the user to do research on the markets above and beyond ‘just backtesting’.

- Detail Results Analysis: best in class analysis tools, including drill-down capabilities into individual strategy results, view trades on charts, write custom metrics and so on.

- Data Integration: RealTest integrates seamlessly with data providers like Norgate Data. Everything is taken care of so you can start building strategies on highly accurate data, without survivorship bias, right away. Supports Stocks, ETFs, Futures and FX.

- Order List Generation: easily generate orders for live trading.

We're not affiliates! We just love the software.

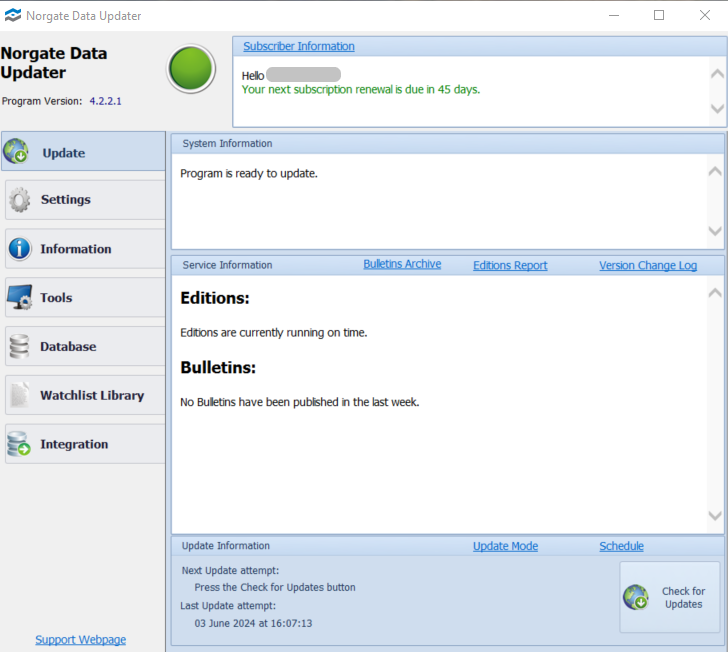

Norgate - clean data

High quality data is paramount

Norgate data is exceptional quality, value for money, and integrates directly with RealTest, Python & other backtesting engines. Specialising in survivorship-bias free data, they cover the US, Australian & Canadian stock markets, as well as selected futures, forex & other data. You literally cannot get off the ground with quant trading unless your data is first rate.

There is no intra-day data, but end-of-day data is extensive, with US stock data going back to 1950, over a 100 futures markets, spot FX, global indeces and much more. Naturally it updates daily for live trading.

We’ve trialled a lot of data suppliers over the years and no one comes close to Norgate for quality, pricing, service or ease of use.

Key features

- Comprehensive Historical Data: with an extensive history, index constituent information and de-listed stocks, Norgate is a one-stop-shop for all you need in this space.

- Data Quality & Adjustment: stocks can be adjusted using multiple methodologies to manage corporate actions like stock splits & dividends. For futures data, back-adjusted & unadjusted continuous contracts are provided.

- Automatic Updates: running in the background, your historic data is kept up to date automatically as it becomes available.

Frequently Asked Questions

Using Python for backtesting?

If you’ve never coded or back-tested before, we’d recommend using something like RealTest before investing thousands of hours into becoming a Python guru. You may not even decided to proceed with trading! However, if you are ready to get going with Python the best place to start is with the courses provided by Tom Starke.

Is automated trading unmonitored trading?

Absolutely not. Full automation means you can avoid the grunt work, but you still need to watch everything closely. To help with this Algo Terminal sends emails and reports so you are alerted to any problems.

What can't RealTest do?

RT handles equities, futures, fx & crypto just fine, but only with End-Of-Day data (daily bars). There is not (yet) capability to backtest on intraday data. It’s also not the application you want for fancy charting. Finally, because RT uses a scripting langugae of its own, there are some limitations in bespoke programming, however, we have almost never found this to be a limitation for the creative thinker. Given how well it does multi-strategy, portfolio testing, it’s very much worth it.

What can't Norgate do?

Norgate presently is all you’d ever need for end of day stock trading, but like RT, there is no intraday data. Forex and economic data are also available and so is futures data, although you should compare and contrast to CSI for futures data depending on your exact requirements.

Other popular back-testing applications?

Amibroker is a popular alternative to RealTest, particular for intra-day systems. For futures and currency traders of course Trade Station is popular, although we feel Multi-Charts is a much better alternative. Strategy Quant-X is an extremely powerful optimization & backtesting tool, but beware of using it to simply over-fit the data. Python tools are everywhere if you want to use them for back-testing, but this is obviously a lot more work. For reasons more related to brokers than productivity, MT4 and MT5 remain popular tools. We don’t recommend them.

Naturally Trade View is always handing for charting and monitoring the markets for free.

For more on the topic, check out the post and podcast here: Episode 24 – Battle of the backtesters.

Other data sources?

This list will get you started. See Quantpedia.

How difficult is it to get started? I'm not a programmer!

It doesn’t have to be that difficult, you probably need 6 months of say 5-10 hours a week to really get moving. You’d start with our introductory courses, use the software we recommend, perhaps jump into one of our more advanced courses and you become relatively proficient in no time.

It helps of course if you are analytical, enjoy tinkering with data in analysis projects and really have a desire to crack it. It’s best to start with a simple project so you have a purpose, a problem to solve. Jump into the Algo Collective community to get started asking questions.